Endowment

EndowmentNorth Carolina lawmakers interested in changing the franchise tax should reform — not cut it or eliminate it — in order to preserve investments in education, roads and bridges, health care, recreation facilities, and other building blocks of a thriving economy that the tax makes possible. Doing so is far more important to the state’s long-term economic prospects than any trivial boost such a tax cut might generate.

Senate leaders have introduced legislation that would reduce the franchise taxes paid on each $1,000 in net worth while setting rates for different types of businesses and those in different industries.1 Bill sponsors have stated that their intent is to pursue complete elimination of the franchise tax in future years.2 The outright elimination of the franchise tax would result in a loss of more than $670 million3 and deliver yet another corporate tax break that is unlikely to change economic performance, ensure North Carolinians have good jobs, or strengthen commercial activity in our communities.

The franchise tax plays a vital role as an alternative minimum corporate tax that funds important priorities across the state. If a corporation manages to zero-out its corporate income tax liability because of tax breaks and loopholes (like single sales factor apportionment, a wide array of tax credits or the absence of mandatory combined reporting), the franchise tax ensures that corporation will pay a modest amount of tax to the state to support the state services and infrastructure from which they benefit – like the skilled workforce produced by state K-12 and higher education programs and the roads that enable corporations to get their products to customers. And the amount of franchise tax liability is modest, according to the latest data for tax year 2016, averaging just $628 annually for S corporations and $8,400 for C corporations.4

Rather than reduce or eliminate the franchise tax, it is time that North Carolina policymakers develop a comprehensive plan for how businesses will contribute to their communities through taxes. This plan must recognize that the reduction in the corporate income tax rate has significantly reduced revenue and shifted the tax load onto individual taxpayers.

Businesses in North Carolina pay lowest taxes in the country

Cutting North Carolina business taxes further won’t make the state’s tax structure more “competitive.” The corporate income tax rate has already been slashed from 6.9 percent to 2.5 percent between 2014 and 2019, and, as a result, in FY 2017, North Carolina was already tied with Indiana for having the second-lowest business tax levels of any state – 3.5 percent of gross state product.5

Tax cuts for businesses since 2013 that have not been limited to the corporate income tax rate; they include changes to the ways that income is apportioned for the purposes of taxation and a range of additional changes to business contributions in other non-General Fund areas like unemployment insurance taxes and privilege taxes. This has meant fewer dollars for the programs and services our communities need to thrive. Proponents of this approach have argued that these tax cuts were necessary to stimulate the economy and job growth. However, tax cuts for businesses have only modest employment impacts in the long-run and only if revenue losses resulting in cuts to other areas do not occur as a result.6 Moreover, research has shown that for businesses to thrive and create jobs, tax policy is a poor tool to support the expansion and creation of firms.7

North Carolina faces a host of unmet needs in our classrooms, in our communities, and for our families. The state’s current tax code and the approach that would continue to reduce taxes paid by businesses is undermining the well-being of North Carolinians, from school capital needs to classroom supplies and supports, to public health protections and health care access, to the water and sewer infrastructure that stewards our natural resources and supports the health of families.

Franchise tax can serve as a minimum tax for businesses

The franchise tax is paid by most businesses operating in North Carolina and can be thought of as an alternative minimum tax paid by businesses in light of cuts to the corporate income tax. The revenue collected supports shared priorities like educating each child and protecting the health and well-being of families.

The annual collection from franchise tax was roughly $670 million, equivalent to more than what is needed to get North Carolina’s per pupil spending back to pre-Recession levels.

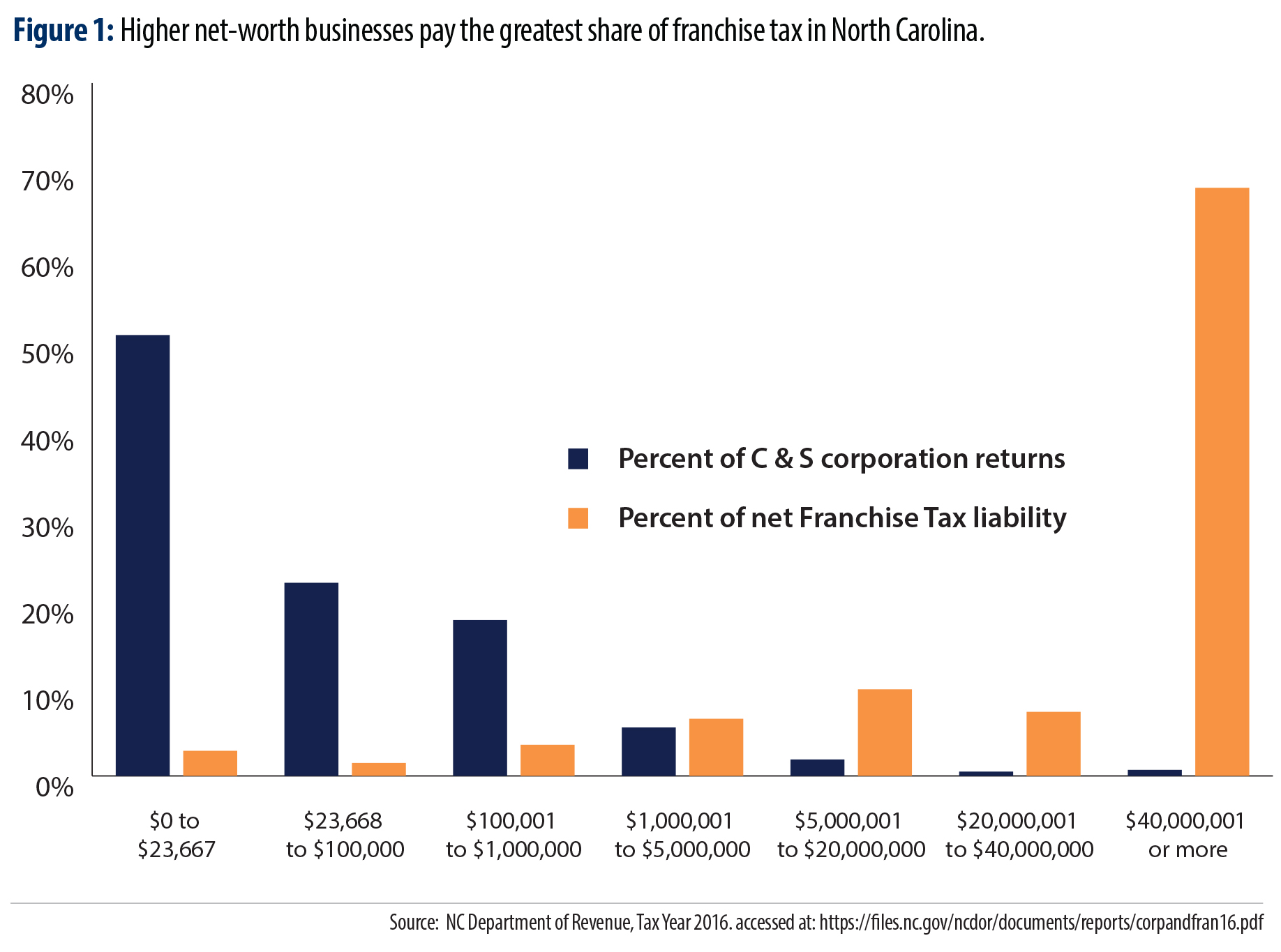

The greater the assets held by a business, the higher the tax. The tax is applied to the companies’ net worth defined broadly as the total assets minus total liabilities.8 In tax year 2016, 75 percent of franchise tax collections came from businesses with net worth calculated at $20 million or more.9

Senate Bill 622 proposes changes to the rate of franchise tax for certain companies. These changes would lower the amount paid from $1.50 per $1,000 to $1.30 per $1,000 while keeping in place the minimum payment of $200 and the cap of $150,000. Electric companies would continue to pay at the higher rate of $1.50 per $1,000. The result is an estimated $140 million annual revenue loss.10

Proponents for the elimination of the franchise tax argue that this is double taxation. However, in most cases, claims of “double taxation” resulting from the franchise tax are bogus. The franchise tax is taxing assets, not income. Given that and the way in which income is now apportioned for state tax purposes, the franchise tax is not being applied to the same base as other taxes. The corporate income tax doesn’t apply to S corporations at all, even though their owners enjoy the complete limited liability that C corporation owners do. And 51.8 percent of C corporations had zero income tax liability or received net refunds in tax year 2016.11 Claims of “double taxation” are a red herring in any case, because multiple taxation is common throughout state and local tax systems.

Reforms to improve the franchise tax should be pursued guided by the principle of revenue neutrality

Any effort to reduce or eliminate the franchise tax must be revenue neutral and seek to raise the equivalent dollars from businesses only, not North Carolina’s working families.

To do so, lawmakers could:

- Expand the businesses subject to the franchise tax to include Limited Liability Companies; this corporate structure is proliferating in the state but not generally subject to the franchise tax – even though it is very similar to S corporations, which are subject to the tax.

- Raise the corporate income tax rate back to 5 percent. The erosion of corporate income tax collections has contributed to the inability of the tax code to deliver on current service commitments and fully meet needs identified as urgent in communities across the state.

- Adopt mandatory combined reporting. 12 Mandatory combined reporting is of particular importance to ensure that corporations that operate in multiple jurisdictions and have profits don’t use separate accounting to avoid paying taxes.13

- Change the way corporate income and assets are apportioned for the purposes of applying the tax rate (also known as eliminating the current single sales factor).14 Apportionment of corporate income can play an important role in the treatment of different businesses and heavily weighting certain factors can lead to inequities in the tax code. A single sales factor apportionment is more likely to benefit companies whose businesses produce goods and services over businesses whose goods and services are sold in local markets.15

- Eliminate corporate tax loopholes that have not demonstrated economic benefits. The state continues to spend through the tax code in ways that benefit certain industries and economic activities. This tax code spending is reported on every two years, and specific items should be more deeply analyzed for the broad economic returns and eliminated should they fall short.16 Specifically, there are a number of tax credits that are applied against the franchise tax liability, and the most recent data suggests that nearly 92 percent of those are claimed by businesses with net worth above $40 million.17

Ensuring that businesses continue to pay the taxes that help our communities thrive is critical to our goals for a strong state economy and the well-being of North Carolinians. Legislators considering proposals to eliminate the franchise tax must ensure that they are considering the ways in which this will shift the tax load further onto individual taxpayers and make it more difficult to invest in the education, health, and well-being of families.

Footnotes

- Senate Bill 622, NC General Assembly 2019, Accessed at: https://www.ncleg.gov/Sessions/2019/Bills/Senate/PDF/S622v0.pdf

- WRAL, April 4, 2019. “Major Tax Cut Pitched in Legislature.” Accessed at: https://www.wral.com/major-business-tax-cut-pitched-in-legislature/18305240/?userId=08399d103fd545089a1cec8ad1f65600

- Based on 2017-2018 collections of franchise tax report by the NC General Assembly, Fiscal Research Division. Accessed at: https://www.ncleg.net/FiscalResearch/generalfund_outlook/18-19/August%202018%20General%20Fund%20Revenue%20Update.pdf

- North Carolina Department of Revenue, Tax Year 2016. Corporation Income and Business Franchise Taxes: Statistics and Trends. Accessed at: https://files.nc.gov/ncdor/documents/reports/corpandfran16.pdf

- COST, November 2018. State and Local Business Taxes. Accessed at: https://cost.org/globalassets/cost/state-tax-resources-pdf-pages/cost-studies-articles-reports/FY16-State-And-Local-Business-Tax-Burden-Study.pdf.pdf

- Bivens, Josh and Hunter Blair, May 2017. ‘Competitive’ distractions: Cutting corporate tax rates will not create jobs or boost incomes for the vast majority of American families. Economic Policy Institute: Washington, DC. Accessed at: https://www.epi.org/publication/competitive-distractions-cutting-corporate-tax-rates-will-not-create-jobs-or-boost-incomes-for-the-vast-majority-of-american-families/

- Mazerov, Michael and Michael Leachman, February 2016. State Job Creation Strategies Often Off Base. Center on Budget and Policy Priorities: Washington, DC. Accessed at: https://www.cbpp.org/research/state-budget-and-tax/state-job-creation-strategies-often-off-base

- Guidance on the franchise tax base and rates can be found here: https://www.ncdor.gov/taxes/franchise-tax-information/net-worth-base-gs-ss-105-122b-applicable-tax-years-beginning-or-after-january-1-2017 and here: https://www.ncdor.gov/taxes/franchise-tax-information/net-worth-base-gs-ss-105-122b-applicable-tax-years-beginning-or-after-january-1-2017

- North Carolina Department of Revenue, Tax Year 2016. Corporation Income and Business Franchise Taxes Statistics and Trends. Accessed at: https://files.nc.gov/ncdor/documents/reports/corpandfran16.pdf

- WRAL, April 4, 2019. “Major Tax Cut Pitched in Legislature.” Accessed at: https://www.wral.com/major-business-tax-cut-pitched-in-legislature/18305240/?userId=08399d103fd545089a1cec8ad1f65600

- North Carolina Department of Revenue, Tax Year 2016. Corporation Income and Business Franchise Taxes: Statistics and Trends. Accessed at: https://files.nc.gov/ncdor/documents/reports/corpandfran16.pdf

- McLenaghan, Edwin, June 2011. Shutting Down Corporate Tax Shelters. BTC Brief: NC Justice Center, Raleigh, NC. Accessed at: https://www.ncjustice.org/publications/shutting-down-corporate-tax-shelters-north-carolina-should-follow-the-lead-of-other-states-by-adopting-key-corporate-tax-reform/

- ITEP, February 2017. Combined Reporting of State Corporate Income Taxes: A Primer. Accessed at: https://itep.org/combined-reporting-of-state-corporate-income-taxes-a-primer-1/

- Johnson, Cedric, March 2014. Tax Change for Multistate Corporations: A Measure that would Harm Critical State Investments and Fail to Help Economy. Accessed at: https://www.ncjustice.org/publications/tax-change-for-multistate-corporations-a-measure-that-would-harm-critical-state-investments-and-fail-to-help-economy/

- ITEP, August 2012. Corporate Income Tax Apportionment: Single Sales Factor. Accessed at: https://itep.org/wp-content/uploads/pb11ssf.pdf

- NC Department of Revenue, 2017. Biennial Tax Expenditure Report. Accessed at: https://files.nc.gov/ncdor/documents/reports/nc_tax_expenditure_report_2017.pdf

- North Carolina Department of Revenue, Tax Year 2016. Corporation Income and Business Franchise Taxes: Statistics and Trends. Accessed at: https://files.nc.gov/ncdor/documents/reports/corpandfran16.pdf