Endowment

EndowmentState, local leaders must find ways to stablize small businesses and to provide support for all owners — Black, brown or white

The United States’ failure to control the spread of the coronavirus and federal leaders’ unwillingness to move quickly with stabilizing economic supports has left no doubt that an economic recovery from the COVID-19 recession will take some time. Businesses owned by people of color face a particularly daunting path to recovery, given their concentration in impacted industries, pre-existing financial precariousness attributable to structural racism, and barriers that have prevented them from accessing available aid.

As North Carolina looks to stabilize its small businesses and build back better than before, state and local leaders will need to account for long-standing inequities that could jeopardize the recovery of businesses owned by people of color, prioritizing policies and models that provide accessible relief while laying the foundation for more equitable small business development in post-pandemic North Carolina.

Pre-existing inequities make minority-owned businesses particularly vulnerable to recessions

Previous experience has shown businesses owned by people of color to be particularly vulnerable to recessions, with white-owned businesses significantly more likely to have survived the Great Recession than Black-owned businesses. As the Brookings Institute notes, a particular facet of inequitable access to capital fueled this disparity in 2008: “Black owners were more reliant on home equity to provide capital for their business and were therefore more exposed as housing prices declined.”[1]

Inequitable access to capital continues to jeopardize the survival of these businesses during the COVID-19 recession. Initial survey data from McKinsey indicate that minority-owned small businesses are more likely to be “extremely” or “very concerned” about the financial viability of their business during the pandemic and are more likely to have conducted layoffs or furloughs or to have shut down their business. Minority-owned businesses also entered the pandemic less able to withstand financial distress; Black- and Latinx-owned small businesses were about twice as likely to be classified as “at risk” or “distressed” than white-owned small businesses.[2]

Researchers have also documented that businesses owned by people of color were more likely to be concentrated in service industries, including accommodation and food services, personal and laundry services, and retail, that were forced to shut down at the onset of the pandemic. In a layering of inequities, the pre-existing financial precariousness of Historically Underutilized Businesses (HUBs) of color is impeding them from accessing available state and federal aid, despite being overrepresented in the most affected sectors.

Economic relief is not reaching businesses owned by people of color

While federal policymakers moved quickly in March to provide relief to small business owners through the Paycheck Protection Program (PPP) and other federal measures, a failure to account for pre-existing inequities may have prevented business owners of color from accessing aid. The PPP largely relied on traditional banking institutions to approve borrowers and distribute loans. As the Brookings Institute has noted, this decision allowed for large-scale rapid relief, but it disadvantaged unbanked and underbanked minority-owned businesses, which are less likely to have relationships with traditional lenders.[3] The PPP’s design also incentivized lenders to push larger and wealthier clients to the front of the line.[4]

Because policymakers did not require borrowers to report demographic information, it is difficult to determine the distribution of PPP loans according to the race or ethnicity of the business owner. The SBA reports that demographic information was reported for only 1 in 4 PPP loans.[5] Survey data from early May nevertheless indicates that sufficient aid is not reaching businesses owned by people of color: Only 12 percent of Black and Latinx small business owners who applied for federal relief have reported receiving the amount they requested, while 26 percent said they had received only a portion of what they had requested.[6] Nearly half of the owners said they expected to close permanently within the next six months.

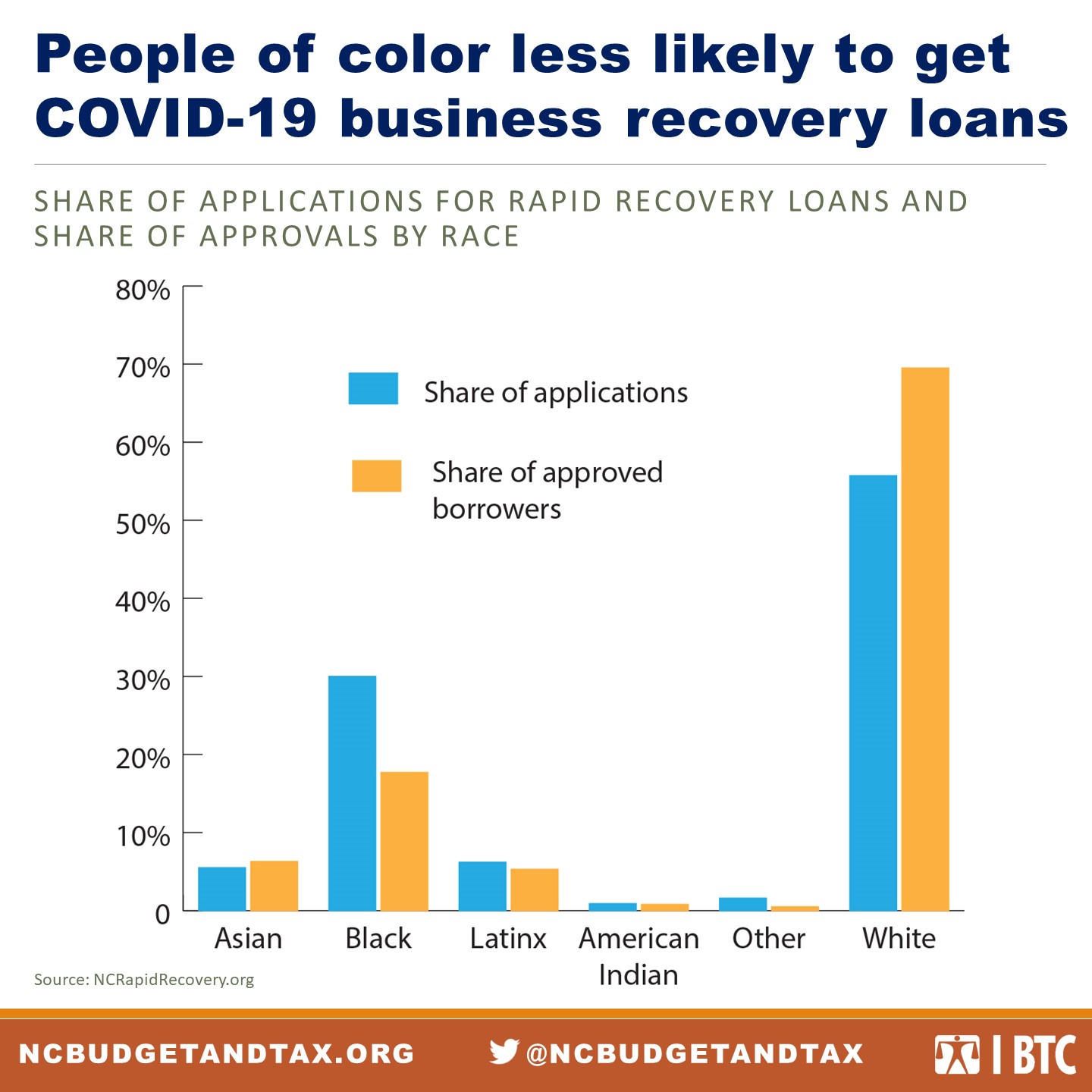

North Carolina’s Rapid Recovery Loan program provides another source of aid for small businesses that have been hard hit during the pandemic, and the program has distributed $35 million in loans to 996 borrowers. The program — which has received appropriations from the General Assembly and is coordinated by the Golden Leaf Foundation and the North Carolina Rural Center — has improved upon federal efforts by collecting and publicly reporting the demographic information of both applicants and approved borrowers. Importantly, loans are made through Community Development Financial Institutions (CDFIs), which are more likely to have established relationships with businesses owned by people of color, and plans were made to intentionally conduct outreach to businesses owned by people of color through trusted institutions.

Preliminary Rapid Recovery data as of Aug. 11 indicate that while loans are reaching certified HUBs, long-standing inequities may still be preventing relief from flowing to HUBs of color. While 64 percent of approved borrowers were minority- or female-owned HUBs, 30 percent of approved borrowers were people of color.[7] Black business owners accounted for 30 percent of applications but only 18 percent of approved borrowers (see Figure 1). Initial reporting has found that most rejected businesses would not have been able to repay a similar loan prior to the pandemic,[8] indicating that a lack of assets and collateral may again be undermining the economic resiliency of HUBs of color.

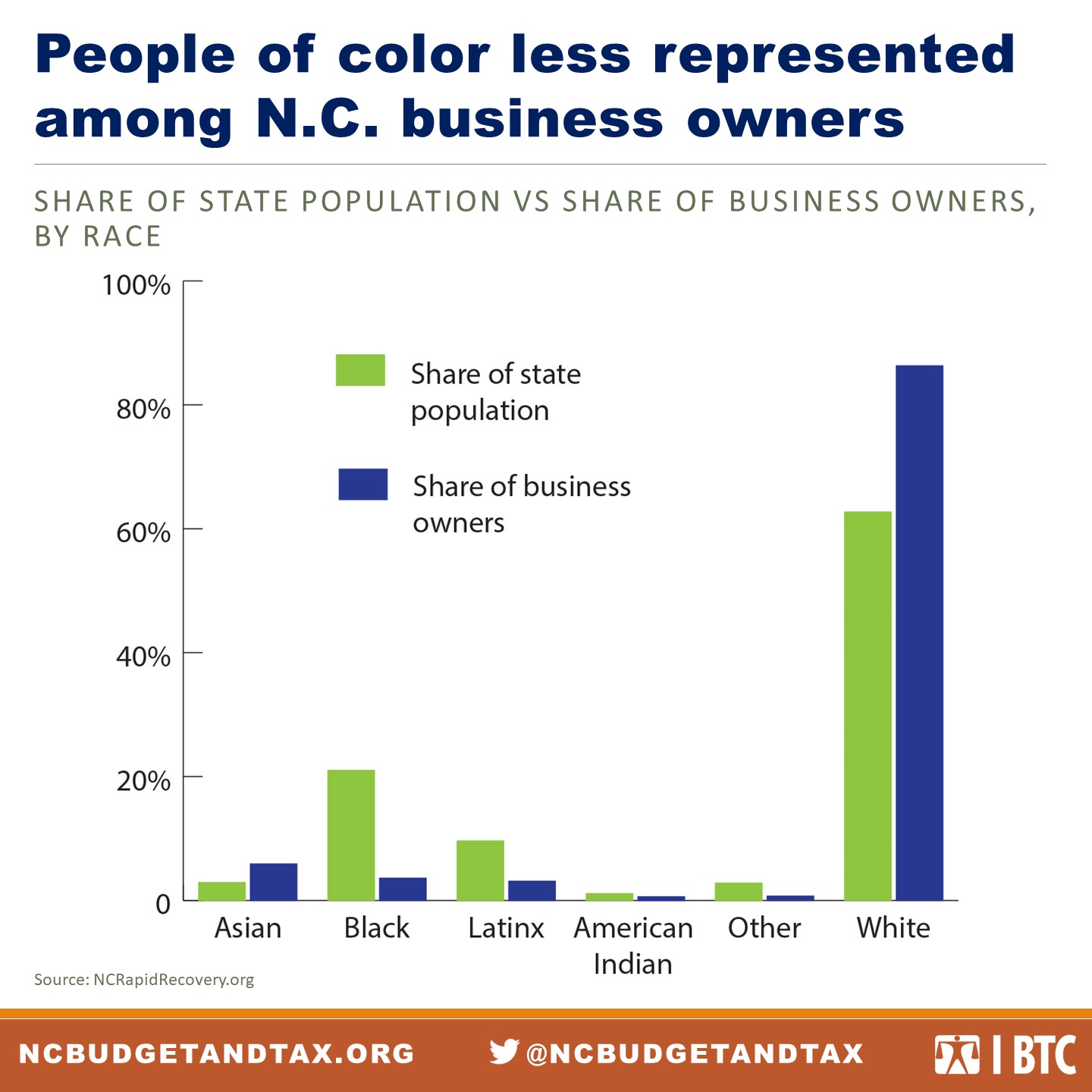

Most strikingly, although people of color received a higher percentage of loans relative to their representation among business owners statewide, this state-wide baseline is incredibly low. Even before the pandemic, North Carolinians of color faced structural barriers to developing and growing businesses: More than 1 in 3 people in North Carolina is a person of color, but fewer than one 1 in 7 businesses in the state is minority-owned. The number of missing Black-owned businesses is particularly stark, with Black North Carolinians accounting for 21 percent of the state’s population but a mere 3.6 percent of its business owners (see Figure 2).

Local policymakers can target small business relief and lay the groundwork for building back better

Foremost concerns for state and local leaders should be the scarcity of businesses owned by people of color in North Carolina and the persistent structural barriers in access to aid during economic crises that cannot be overcome by outreach. Initial data from the Rapid Recovery Program demonstrate the need to address these underlying structural issues with more grant opportunities rather than loans and with deeper technical assistance to businesses owned by people of color. North Carolina’s policymakers should develop model programs and policies that explicitly seek to engage with businesses owned by people of color and to support their recovery from the COVID-19 recession. As analysts from McKinsey have noted:

“Immediate relief in the form of grants, loans, subsidized access to legal advice, professional assistance to negotiate with creditors or landlords, and free-advertising credits could help minority-owned small businesses respond to the pandemic and protect their employees. Community-relief funds could provide short-term support to businesses with reduced revenues. Large companies could also offer emergency grants to support small businesses in crisis.”[9]

Many local governments have already begun this work in their pandemic responses, including through the establishment of small business assistance funds that offer grants in addition to loans in Durham, Raleigh, and Orange County. To address underlying inequities in access to capital and other barriers to business development, local leaders can look to the experiences of communities that were developing models to better support HUBs even before the onset of the pandemic. This work includes efforts to increase access to capital in Charlotte, provide technical assistance in Durham, and expand contracting in Asheville. North Carolina policymakers can build on this progress to ensure immediate access to urgently needed relief while laying the foundation for the state’s small businesses to build back stronger and more equitable than before.

[1] Joseph Parilla and Sifan Liu, “Businesses Owned by Women and Minorities Have Grown. Will COVID-19 Undo That?,” Brookings (blog), April 14, 2020, https://www.brookings.edu/research/businesses-owned-by-women-and-minorities-have-grown-will-covid-19-undo-that/.

[2] André Dua et al., “COVID-19’s Effect on Minority-Owned Small Businesses” (McKinsey & Company, May 27, 2020), https://www.mckinsey.com/industries/public-and-social-sector/our-insights/covid-19s-effect-on-minority-owned-small-businesses-in-the-united-states.

[3] Parilla and Liu, “Businesses Owned by Women and Minorities Have Grown. Will COVID-19 Undo That?”

[4] Joyce M. Rosenberg, “Head of the Line: Big Companies Got Coronavirus Loans First,” Washington Post, July 20, 2020, https://www.washingtonpost.com/business/size-mattered-big-companies-got-coronavirus-loans-first/2020/07/20/14393d72-ca97-11ea-99b0-8426e26d203b_story.html.

[5] “Paycheck Protection Program (PPP) Loan Data – Key Aspects” (Small Business Administration, n.d.), https://www.sba.gov/sites/default/files/2020-07/PPP%20Loan%20Data%20-%20Key%20Aspects-508.pdf.

[6] Global Strategy Group, “Federal Stimulus Survey Findings” (Prepared for Color of Change and Unidos US, May 2020), https://theblackresponse.org/wp-content/uploads/2020/05/COC-UnidosUS-Abbreviated-Deck-F05.13.20.pdf.

[7] “News & Updates – NC Rapid Recovery,” NC Rapid Recovery, August 11, 2020, https://ncrapidrecovery.org/news-updates/.

[8] Colin Campbell, “NC Legislature’s Coronavirus Business Loans Provide Millions,” Raleigh News & Observer, July 31, 2020, https://www.newsobserver.com/news/politics-government/article244602472.html.

[9] Dua et al., “COVID-19’s Effect on Minority-Owned Small Businesses.”