Endowment

EndowmentHigher tax rates on very high incomes have been raised as a policy option at the national level as a means to finance key investments and plans to ensure the sustainability and environmental health of our nation, as well as address growing income inequality. But federal policymakers aren’t alone in being able to consider such a graduated rate structure on income as a way to strengthen investments in communities; state leaders across the country are considering — or have already implemented — higher tax rates on high incomes.

For North Carolina, a graduated tax structure that taxes higher incomes at higher rates could serve as one tool to raise revenue for priorities in communities across our state to support access to opportunity. It would also address, in part, the state’s upside down tax code.

Marginal Taxes: How They Work, and Why They Matter

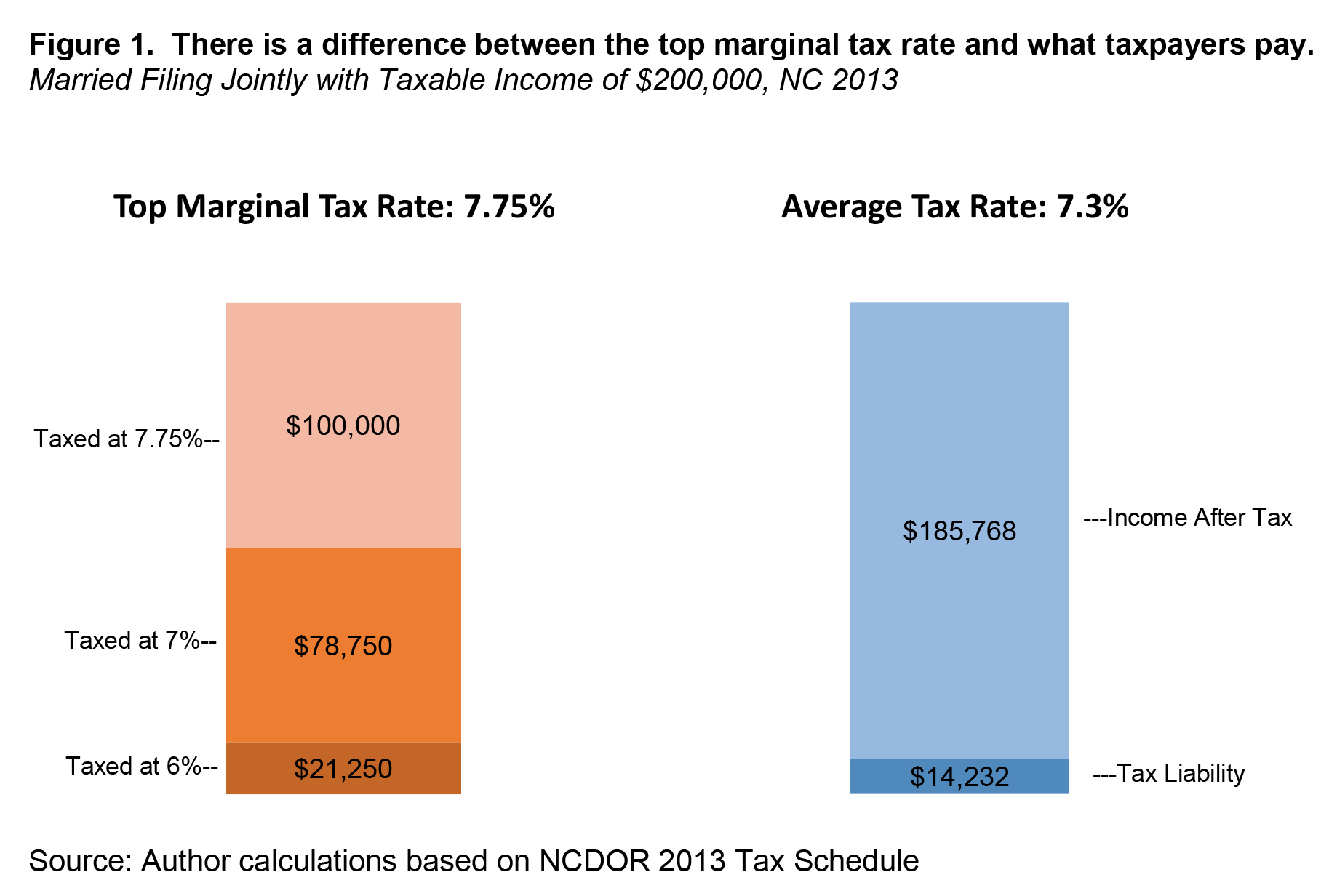

It is worth reviewing what exactly is proposed by taxing higher incomes at higher rates. Marginal tax rates are imposed on each additional dollar of income after a pre-determined income threshold. It does not make each dollar held by a taxpayer subject to that rate. Moreover, the marginal tax rate is not equivalent to the effective (or average) tax rate which is the share of income paid in taxes after all deductions and credits are applied.1 A taxpayer’s marginal tax rate, particularly the top marginal rate, is usually higher than their effective tax rate.

As an example of how marginal tax rates work, before the 2013 tax changes in North Carolina’s tax code, a taxpayer with $200,000 in taxable income (those in the top 20 percent of taxpayers) would have only paid the top marginal tax rate of 7.75 percent on their income over $100,000.2 This higher rate results in paying $960 more on the taxpayer’s second $100,000 in income than the taxpayer paid on the first $100,000. In the long-run, establishing both higher rates on higher income and ensuring higher effective tax rates for the rich must be pursued, as this limits the ability for deductions to erode the tax base.3

Researchers have proposed higher marginal tax rates on higher incomes based on the idea that $1 for a very wealthy person doesn’t make a significant impact on their well-being in the same way that it would for someone with much lower incomes.4

At the same time, a graduated rate structure — in contrast with the state’s current flat tax rate on income — can make more revenue available for key public investments, generating broad-based benefits to many people and communities. It is also better able to keep up with the needs of a growing state. That is because graduated rates do a better job aligning with where income is concentrated and growing.5

Recent research finds that states that have increased their top income tax rates have done so without harming their economies. The majority of states that raised taxes had growth roughly equaling or exceeding neighboring states.6

A Millionaire’s Tax in North Carolina

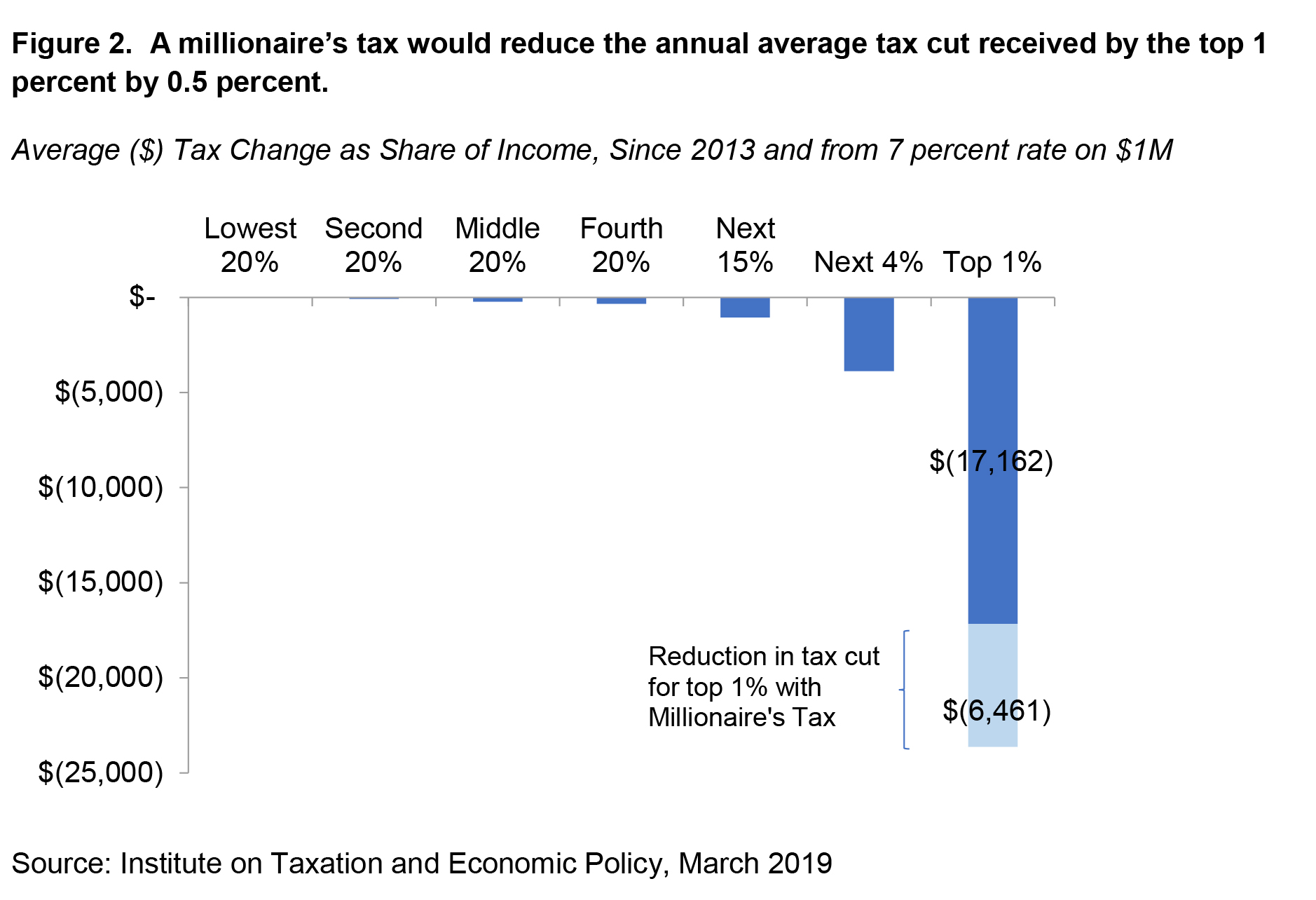

Due to the adoption of the flat income tax rate that has reduced to 5.25 percent since 2013, the top 1 percent whose income is over $1 million receives 28 percent of the annual net tax cut.7 The average annual tax cut for the top 1 percent in 2019 is estimated at $23,600 (see Figure 2.)

A higher marginal tax rate on income over $1 million would reduce the size of the average net tax cut for the top 1 percent by 0.5 percent, or $6,461. This would, in part, address the upside-down nature of the tax code while making it less likely that the tax load will continue to shift to low- and middle-income taxpayers as growing needs must be met. Future policymakers would not be inclined to just raise the flat rate on all income but could continue to build a graduated rate structure on higher income.

A graduated rate structure, particularly one that places a top marginal rate on income over $1 million, would make revenue available for priorities in communities across the state like supporting classroom investments, water quality, and monitoring and creating a more affordable post-secondary education system. Roughly $362 million could be raised from a millionaire’s tax in North Carolina.8

North Carolina’s tax code is not keeping up with our growing needs. Although our state seeks to provide each of us with a high quality of life, it’s already struggling to keep up with investments needed in the classroom, in the infrastructure that ensures our communities are resilient and connected to opportunity, and in the protections and supports that promote healthy living environments — a problem that will continue to grow in future years unless lawmakers act.

A millionaire’s tax — and moving to a graduated income tax structure that sets higher rates on higher income — can help North Carolina invest to decrease racial inequities, build economic opportunity, and spur growth.

Footnotes

- Center on Budget & Policy Priorities, Policy Basic on Marginal and Average Tax Rates, Accessed at: https://www.cbpp.org/research/federal-tax/policy-basics-marginal-and-average-tax-rates

- “Marginal versus Effective Personal Income Tax Rates” The Budget and Tax Center at the North Carolina Justice Center – https://www.ncjustice.org/wp-content/uploads/2018/12/BTC-Policy-Basic_Marginal-and-Effective-Tax-Rates.pdf

- See more here: https://itep.org/how-to-think-about-the-70-top-tax-rate-proposed-by-ocasio-cortez-and-multiple-scholars/

- Diamond, Peter and Emmanuel Saez, 2012. The Case for Progressive Tax: From Basic Research to Policy Recommendations. Accessed at: https://eml.berkeley.edu//~saez/diamond-saezJEP11opttax.pdf

- Institute on Taxation and Economic Policy, 2011. A Guide to Fair State and Local Taxes.

- Center on Budget and Policy Priorities, “Raising State Income Tax Rates on the Top a Sensible Way to Fund Key Investments,” February 2019 – https://www.cbpp.org/sites/default/files/atoms/files/2-7-19sfp.pdf

- Special Data Request to the Institute on Taxation and Economic Policy, 2018.

- Special Data Request to the Institute on Taxation and Economic Policy, 2018.