Endowment

EndowmentFiscal policy choices have the ability to either deepen — or alleviate — racial disparities.

The COVID-19 crisis has made clear that communities can experience the same events with disparate impacts along the lines of race, ethnicity, and income. Black, Indigenous, and Latinx communities and people with low incomes have been hit hard by the virus; these North Carolinians continue to experience higher death rates, more workplace safety risks, higher job losses, and greater income losses. The health and economic disparities emerging from the pandemic are a cumulative result of inequities and barriers created by policy choices and a history of racism, bias, and discrimination. Policies and public institutions that limit access to education, quality jobs, and intergenerational wealth for communities of color continue to do harm and fuel racial and economic inequities today.

North Carolina’s tax code and budget are wrought with such policy choices, which can result in racist outcomes[1] that worsen barriers to well-being for people and communities of color, according to new data from the Institute on Taxation and Economic Policy (ITEP).[2] The greater tax load carried by Black, Indigenous, and Latinx residents has been exacerbated by state tax policy choices made in 2013, which were layered on historic policy choices that set up a tax code structure that already asked for inequitable contributions from taxpayers of color.[3] By analyzing the impact these policy choices have on different racial and ethnic groups, policymakers could gain clearer insight into the choices that are shaping (and harming) our lives and could make policy choices that advance more equitable outcomes.

This report analyzes the outcomes of who pays taxes in North Carolina and the ways in which our current tax code directly — and via the investments it supports — impacts Black, Indigenous, Latinx, and white residents. Each year, the foundation of our policymaking is often whether and how we will raise collective resources to advance our state’s well-being.

Tax policy, when designed with equity in mind, can support racial justice and sustainable economic growth that delivers broad-based benefits to all.[4] The pandemic has made clear that North Carolina lawmakers can and must make intentional and sound policy choices that respond to the systemic causes of COVID-19’s disparities.

Income inequality compounds racial and ethnic disparities

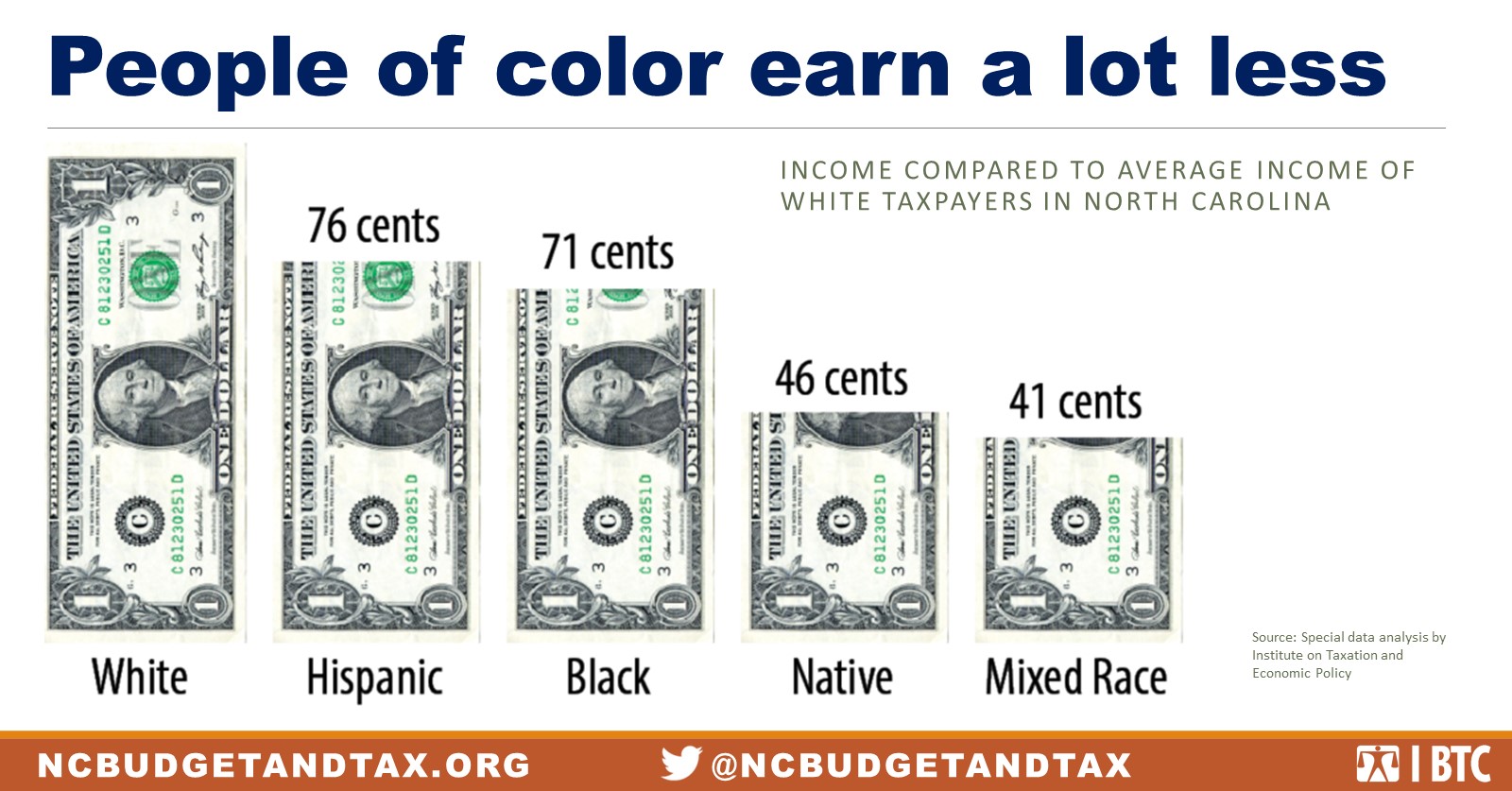

For every dollar that the average white person makes in income, Hispanic people in North Carolina make 76 cents, Black people make 71 cents, Native people make 46 cents, and people of more than one race make just 41 cents.[5]

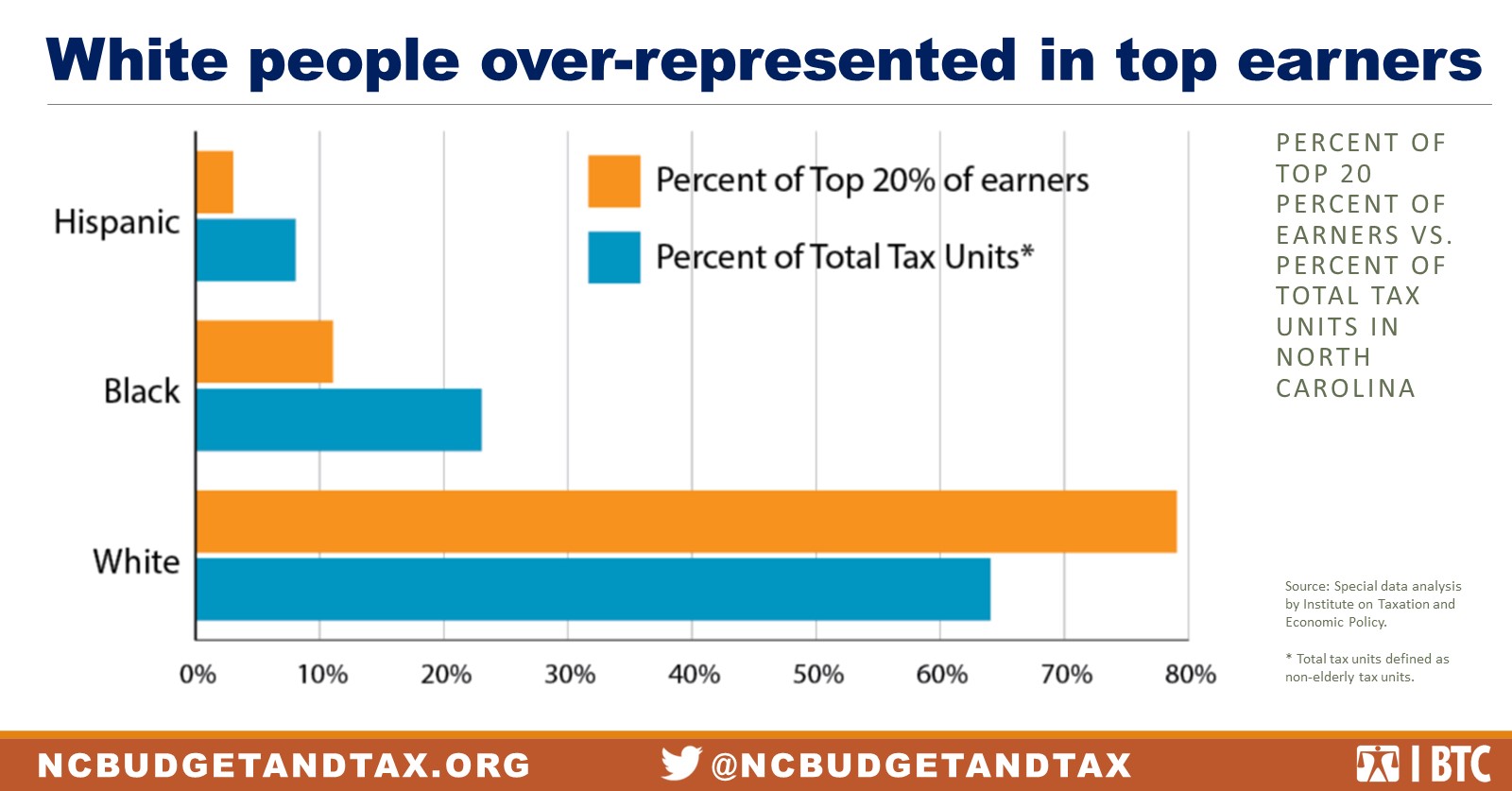

White people are overrepresented among North Carolina’s richest households. About two-thirds of North Carolina’s non-elderly tax filers are white, and 4 out of 5 of the top 20 percent of earners — who report over $91,300 per year — are white.[6]

Income inequality compounds the racial inequities in North Carolina. Labor market discrimination, disparities in educational and work experience, and occupational segregation have meant that people of color work for lower wages.[7] Research has found that even as Black workers have experienced modest wage gains, the relative boost has not overcome the growth of income at the very top. The income distribution itself has been shown to be a significant driver of the racial income gap.[8]

“The effect of rising income inequality on racial disparities also becomes evident by simulating what the income gap would look like if the overall income distribution had stayed constant. If overall inequality hadn’t gone up, the ratio of median black family income to white family income would have climbed from 57 percent to 70 percent, decreasing the racial income gap by 30 percent.”[9]

Historical and current barriers to good jobs, educational opportunities, and asset-building activities like banking and buying homes have caused a disproportionate share of Black and Hispanic households to be pushed into the bottom 20 percent of income earners, making less than $17,800 per year. Black people are just over one-fifth of North Carolina’s non-elderly tax filers but nearly one-third of the bottom 20 percent of tax filers. Whereas white people are nearly two-thirds of tax filers but only just over half of the bottom 20 percent of tax filers.[10]

North Carolina’s tax code is upside-down

North Carolina’s upside-down tax system is failing to address existing inequities.[11]

Families with high incomes, who are disproportionately white, pay lower effective tax rates than families of color with lower incomes. White households in the top 20 percent of filers pay 7.6 percent of their income in taxes each year. Black and Native households in the bottom 80 percent of filers pay about 9 percent of their income in taxes, and Hispanic families in the same group pay 8.7 percent.[12]

Wealthy North Carolinians contribute a smaller share of their income in taxes while those of more modest means are required to contribute more. Families of all races and ethnicities in the bottom 80 percent (those earning less than $91,300 per year) receive just 41 percent of statewide income but pay 46 percent of statewide taxes.[13]

According to ITEP, the top 20 percent of earners receive 59 percent of the total income earned in North Carolina but pay just 54 percent of state and local taxes. White taxpayers in the top 20 percent of earners receive nearly half (47.5 percent) of all income statewide but pay just 44 percent of state and local taxes.[14]

After state and local taxes, income disparities are essentially unchanged. White people’s average income decreases by 0.1 percent while Black people’s average income increases by 0.1 percent after state and local taxes. The average income of Hispanic people is unchanged by state and local taxes. North Carolina’s tax policy should be doing more to equalize incomes across race and ethnicity.[15]

Over the past 50 years, wealth has become increasingly concentrated among a wealthy few. Federal Reserve Chairman Jerome Powell has repeatedly stated that income inequality weighs our economy down, undermines opportunity, and stunts productivity and growth.[16]

“The productive capacity of the economy is limited when not everyone has the opportunity, has the educational background and the health care and all the things that you need to be an active participant in our workforce.”[17]

Tax policy can promote economic growth and shared prosperity

Tax policy can either deepen or alleviate racial disparities. When tax policies exacerbate income inequality and therefore racial disparities, families face increased hardship and the state’s economic potential is stifled.

The primary purpose of taxes is to generate the resources needed to fully fund essential public services and build vital infrastructure — which fuels our state economy.[18]

When we fail to align revenue streams with stainable sources of economic expansion, the tax code by design falls behind in adequately addressing community needs. When our tax code provides exclusions, loopholes, and preferential rates for certain types of wealth, like capital gains[19], it places unnecessary limits on public resources, creates barriers to accessing public services, and stifles economic growth, contributing to inequities rather than addressing them.[20]

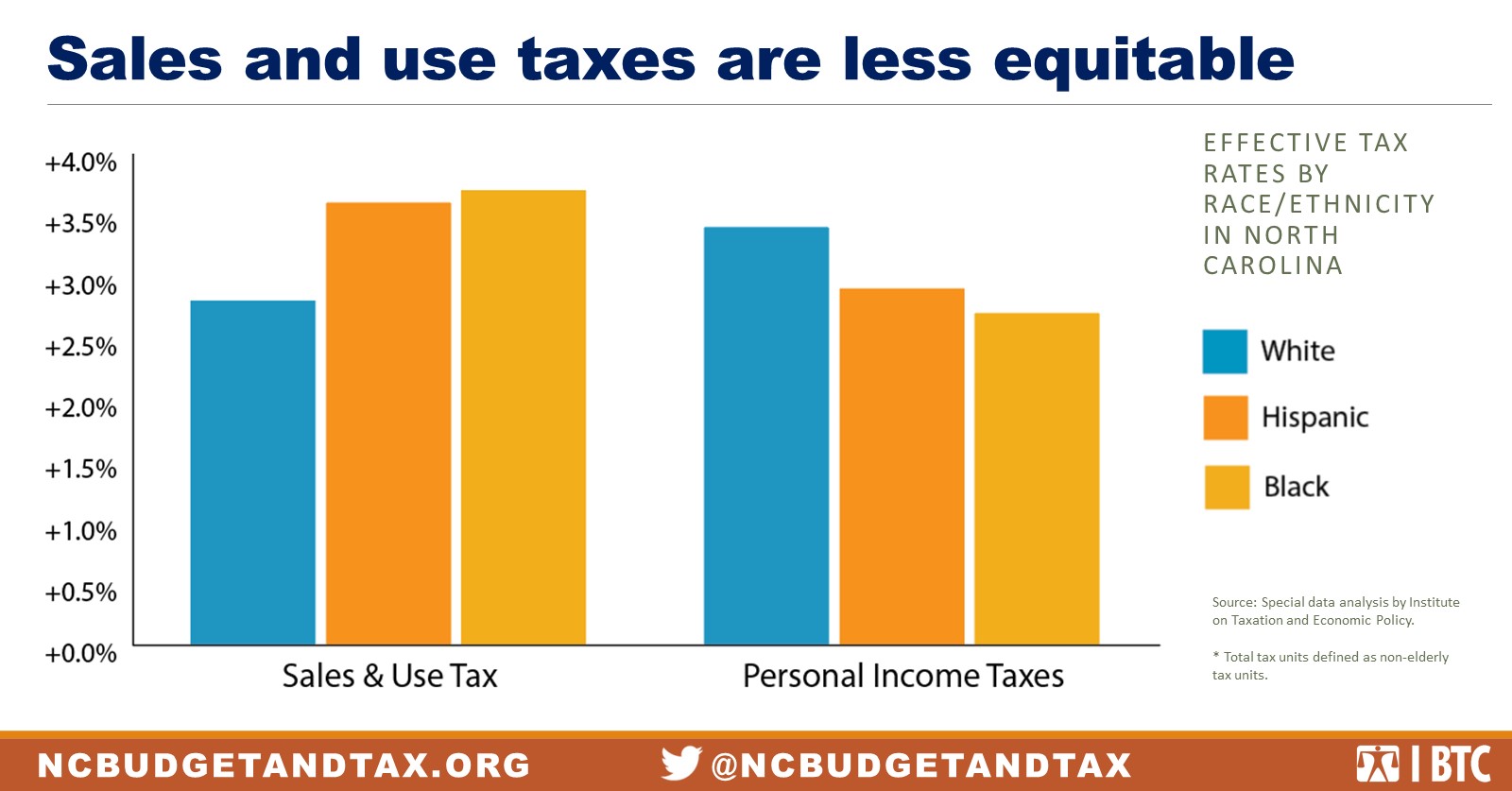

Different taxes have very different impacts by income, race, and ethnicity. North Carolina’s sales and excise taxes, for example, are worsening disparities in income by race and ethnicity. Because people of color are more likely to be lower income groups, these households are spending more of what they earn each month and thus paying more in sales tax as a share of their income. Black households pay an average rate (3.6 percent) that is 20 percent above the state-wide average and 29 percent above white households’ average rate. Hispanic households pay an average rate (3.7 percent) that is 23 percent above the statewide average and 32 percent above white households’ average.

Personal and corporate income taxes, by contrast, can help narrow racial and ethnic income gaps. However, North Carolina currently has a flat personal income tax rate that results in a multimillionaire paying the same rate on their second million dollars as a person moving out of poverty pays on their income above the federal poverty level. Because white families have higher average incomes, their average combined income tax payment (3.4 percent of income) is slightly higher than the rates paid by Black (2.9 percent) or Hispanic (2.7 percent) families.

North Carolina, like the country, designed its tax codes to support the building of wealth for the already wealthy and in so doing often excludes the middle class and penalizes poor households.[21] Such policies in North Carolina include preferential treatment for investment income and inheritances and deductions for mortgage payments.

By choosing tax policies that align with the ability to pay, North Carolina policymakers could reverse the current upside-down tax code to increase consumer purchasing power, boost commerce, equalize access to wealth and well-being, and promote shared prosperity.[22]

State and local tax policy in our region has blocked progress throughout history

Emerging research shows how today’s state and local tax structures were set up throughout the history of the United States to exclude people of color from accessing the public institutions and services that could lead to greater economic opportunities while also protecting the wealth and power of white people.[23] From the adoption of poll taxes and supermajorities to the tax breaks given to property owners and high-income earners, historic records provide a compelling case that North Carolina is not alone in suffering from the fallacy that tax policy is race-neutral.[24]

As a Southern state, North Carolina shares a common set of fiscal structures that require Black, Indigenous, and Latinx people to pay more of their income in taxes than white people. Of the 12 states in the Southeast region, at least five have legislative supermajority requirements to increase taxes, nine have statewide limits on property tax rates, and nine are “Dillon’s Rule” states that limit local governments’ ability to raise revenue. These states are also less likely to have fair (or progressive) income tax structures and refundable tax credits for working families with low or modest incomes.

North Carolina’s own history shows how tax policies — and decisions about how to allocate tax dollars — laid the foundation for outcomes in education, well-being, and asset ownership.[25]

In the Reconstruction period, the North Carolina General Assembly passed legislation to allow white property owners to pay taxes that would fund white schools and taxing Black property owners for schools that would serve Black children. This approach was later struck down by the state Supreme Court, but it fueled the movement of white supremacist political agendas in the decades that followed and had a real impact on the investments in public schools. As the authors of Deep Rooted note, “In 1886 in New Bern, per-pupil spending at the local public schools was $11 per white student, but $5 per black student.”[26]

In 1961, Gov. Terry Sanford proposed the repeal of an exemption of food and medicine from the sales tax to support funding for public education that would be available to every child.[27] The sales tax mechanism was a last resort after other tax options were rejected by legislators. While analysis shows that the state was able to make progress on investment in teacher pay and resources for schools in the period following the enactment of the tax, many remained concerned about the use of a tax that asked more from low-income and communities of color than from higher income and white taxpayers. The promise of an extension of the temporary tax based on a vote of the people did not happen along the initial timeline, and instead efforts to repeal the tax on food were taken up and passed by the NC General Assembly in 1999.

A cap in the state Constitution on income tax rates of 10 percent that was first established in 1868 was meant to set clear limits on tax collection from wealthier white taxpayers. By amendment in 2018, the cap was reduced to 7 percent and further limited the legislature’s ability to establish a graduated rate structure and a tax code that would raise needed revenue.[28] The impact of this change benefits the top 1 percent of taxpayers who saw their tax rate on high income held below previous graduated rate structures.

Recent tax policy choices have made our tax code even less equitable

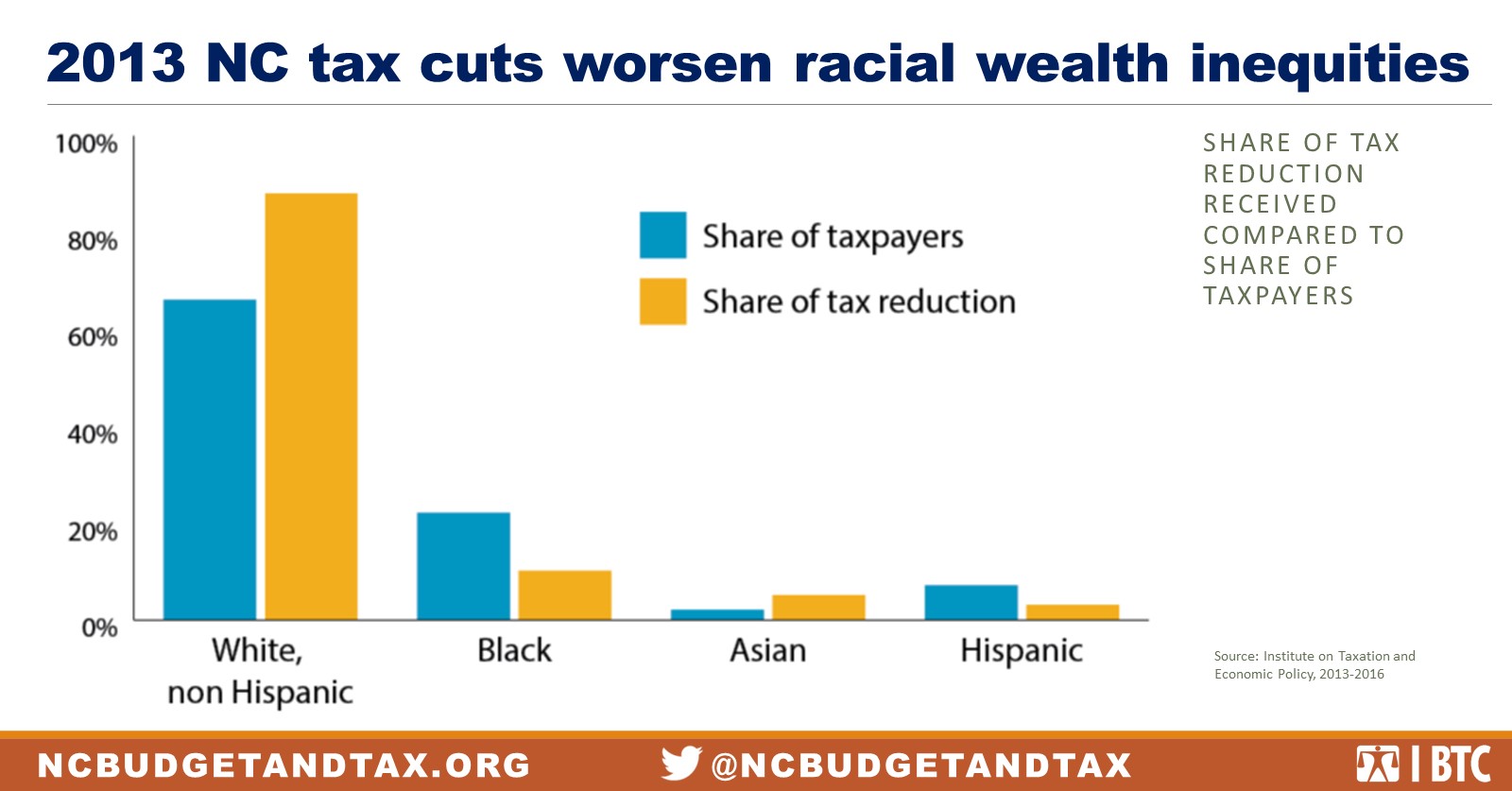

In 2013, North Carolina lawmakers eliminated the state’s Earned Income Tax Credit (EITC), implemented a flat tax rate on personal income, cut the corporate income tax rate, minimally expanded the sales tax base, and eliminated the state’s estate tax, among other changes detailed on page 9-10. As a result of these changes, the state lost nearly $4 billion in the most recent fiscal year. At the same time, the tax changes in 2013 have delivered the greatest tax cuts to white and wealthy taxpayers and have increased racial and economic inequities.[29]

Tax cutting continued throughout the decade, greatly reducing the funding for public investments. North Carolina lawmakers cost the state $151 million when they expanded tax loopholes for profitable corporations operating in multiple states through Passive Income Corporations. They cost the state another $123 million by creating an apportionment formula that lowered corporations’ state tax rates by solely relying on sales in the state for tax calculations rather than equally weighing their payroll, property, and sales. Many other state tax expenditures for corporations also have gone under-scrutinized. Among those not already noted are sales tax exemptions available for luxury purchases; subsidies to industries such as telecommunications and utilities, which underserve communities with lower incomes and rural places in our state; and several carry-forward and depreciation rules that provide additional corporate tax breaks and result in greater state-level losses.

In 2018, revenue-raising capacity in the state was lowered by reducing the constitutional cap on income tax rates from 10 percent to 7 percent. Reversing the 2018 constitutional amendment is a vital long-term reform that would ensure that lawmakers can respond to downturns and adequately fund public services by asking for more from higher-income households with the greatest ability to pay. [30]

Barriers to equity: Estate tax

- Policy Change: Eliminated the state estate tax on estates valued at more than $5.25 million

- Who benefited: Heirs of very wealthy people

- Equity: Exacerbates wealth inequality that is exacerbated by intergenerational wealth transfers

- Impact: Fluctuates annually but estimates suggest $140 million

- Alternative: Reinstate an inheritance tax

Barriers to equity: Flat tax

- Policy Change: Changed from graduated income tax brackets to a flat rate of 5.8 percent in 2014, 5.75 percent in 2015, 5.499 percent in 2017, and 5.25 percent in 2018

- Who benefited: Wealthiest households

- Equity: Disproportionately negative impact on people of color with low incomes

- Impact: Over $1 billion a year

- Alternative: Reinstate graduated income tax brackets

Barriers to equity: Expansion of sales tax base

- Policy Change: The expansion of the sales tax base to more goods and services without lowering the rate happened even as the refundable state Earned Income Tax Credit was eliminated.

- Who benefited: The sales tax base expansion made up for some but not all of the revenue losses from income tax cuts, but very few benefited from this change. Working families lost a refundable tax credit on earned income, and small businesses had to begin collecting sales tax on goods and services.

- Equity: Disproportionately negative impact on North Carolinians with low incomes and people of color

- Impact: Sales tax revenue represents a growing share of overall tax revenue but asks more of low- and middle-income taxpayers as a share of their income

- Alternative: Reinstate a refundable state EITC at least 20 percent of the federal credit

Barriers to equity: Corporate loopholes

- Policy Change: Single sales factor passed in 2015, three-year phase-in period

- Who benefited: Multi-state and multi-national corporations that do business in North Carolina, but the majority of their sales are in other states

- Equity: Large, profitable corporations are able to move in and squeeze out competition from small and historically underutilized businesses

- Impact: Small, BIPOC-owned businesses are forced to compete with the Amazons and Walmarts of the world.

- Alternative: Reinstate three sales factor formula (property, payroll, and sales)

Tax cuts and North Carolina’s austerity budgets

North Carolina’s tax cuts reinforced an austerity budgeting approach during the most recent economic expansion. The state now invests in its communities at 4.54 percent of state personal income, a measure of the size of the total economy that represents a 23 percent decline in spending to provide a foundation for quality of life and economic well-being. If North Carolina was spending at the 45-year average, given the size of the economy today, the state would be investing $5.4 billion more into its communities. Over current year spending, this would mean a 20 percent increase in investment and dollars that could go to specific identified needs like delivering a sound basic education to every child as required by Leandro – the court case which deemed North Carolina’s underfunding of public education unconstitutional.

Tax cuts since 2013 mean that the state has an estimated $4 billion less in revenue each year to make priority investments. Cuts to public programs and services like those described below, which connect people to basic needs and economic opportunities, have made outcomes for historically excluded and marginalized groups worse. Even as a growing body of research points to the potential of targeted public investments to drive more equitable and broad-based improvements in well-being, years of budget cuts have continued to hurt North Carolinians in communities of color and with low incomes. Over the past year, COVID-19 has underscored and worsened the ways in which these budget cuts have disproportionately harmed these communities.

Public health services that connect families to health information, vaccinations, and affordable care have been underfunded for years. North Carolina spends just $61 per person on its network of public health departments, which connect communities of color and those with low incomes to otherwise unaffordable health care. From 2008 to 2018, North Carolina’s population grew by 12 percent while state public health funding fell by 28 percent.[31] These reductions in state spending have long left public health departments under-resourced and communities of color under-served. Data on life expectancy in North Carolina shows that life expectancy for Black North Carolinians is three years less than for white North Carolinians.[32] More recently, budget cuts have left public health departments unable to distribute vaccinations quickly enough to the communities they serve. To date, communities of color continue to do more poorly than white communities in COVID-19 vaccination, infection, and death rates — further emphasizing the dire impacts of North Carlina’s inequitable tax and budget policy choices.[33]

North Carolina has made significant cuts to its early childhood education system and disproportionately harmed children and teachers of color in doing so. Funding for this system is meant to ensure early childhood educators are paid livable wages, keep child care affordable, and make programs accessible to communities across the state. The state not only has reduced its own commitment to child care assistance over the years, but in 2018, additional federal dollars for the expansion of child care opportunities through the Child Care Development Fund Block Grant (CCDBG) were redirected. As a result, fewer North Carolina children receive care, educators earn lower wages, and the state misses out on the benefits of high-quality child care. In North Carolina, over half of early childhood educators are women of color, and the average starting wage for teachers is just $10 an hour.[34] Nationally, Black female early childhood educators who work full time make 84 cents for every $1 earned by their white counterparts.[35] If North Carolina policymakers had simply maintained FY 2008 funding levels, the FY 2018 budget would have been $40.5 million greater. In combination with $50 million in CCDBG expansion dollars, this could have transformed the availability and quality of child care statewide and ensured that more women of color earned a living wage as educators.[36]

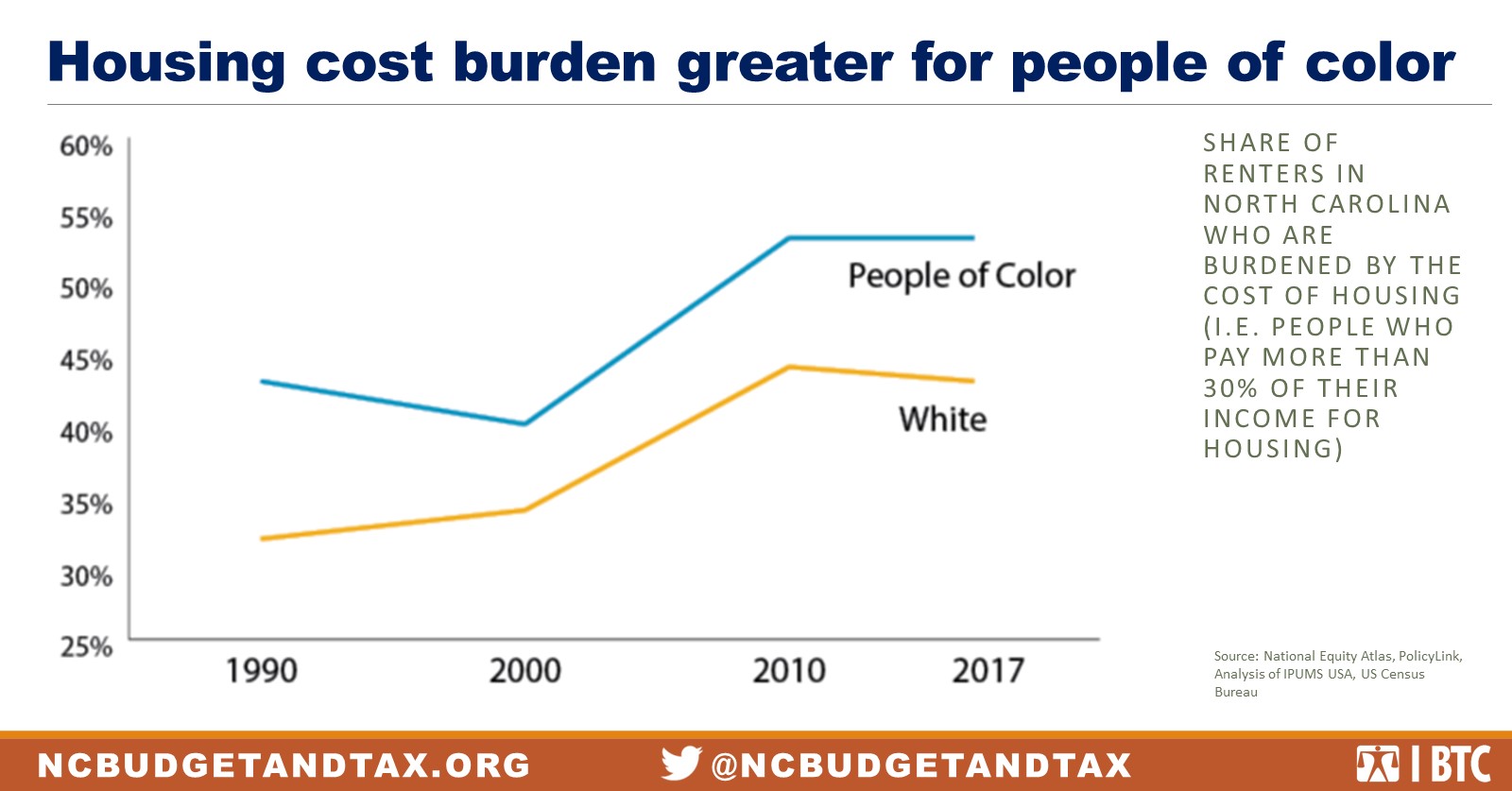

Affordable housing is more likely to be out of reach for communities of color.[37] State support for building out the affordable housing stock has declined in recent years as the state’s Housing Trust Fund has dropped from $22 million in Fiscal Year 2007 to $10 million in state appropriations today. With unaffordable housing options, too many families across the state face difficult choices between paying rent and meeting other basic needs or setting aside dollars for saving. As evidenced in the data on housing cost burden, which is measured as housing costs that represent 30 percent or more of a households income, North Carolina shows a marked increase in housing cost burden overall and a growing disparity in cost burden between households of color and white households.

North Carolina can choose a different way forward

After years of policy choices that have worsened racial and economic inequities, the COVID-19 pandemic has created what could become a defining moment for North Carolina. For the past decade, tax cuts and declining state investments have failed to deliver the broad-based prosperity that was promised, setting the stage for disproportionate harms to Black and Indigenous people and people of color. Unfair fiscal policies have eroded our tax base and have led to health and financial hardship for many while preserving wealth and power for a fortunate and mostly white few. But North Carolina lawmakers can choose a new and better path forward for our communities.

Addressing disparities in income, health, and well-being by race and ethnicity will require North Carolina to adopt a more progressive tax system, with higher tax rates on affluent residents and businesses but comparatively less reliance on taxes from families with low and moderate incomes, who are already paying their fair share. Implementing a graduated personal income tax rate structure, eliminating regressive deductions, strengthening the corporate income tax, removing groceries from local sales tax bases, reducing state and local sales tax rates, and restoring an estate tax on high levels of wealth would all move North Carolina in this direction. Policies designed to lift families out of poverty like tax credits for workers, renters, and families with children also could enhance the racial equity of North Carolina’s tax code.

In times of crisis, the unmet needs of families and communities become more urgent and dire. Growing need for food, shelter, health care, and income could and should be met with greater investments in social services. Ensuring that our fiscal policies support the well-being of every person — Black, brown, and white — is critical to the success of a recovery that delivers prosperity to all. Our policymakers must recognize that targeted public investments backed by antiracist tax policies are the best pro-growth strategy for North Carolina — and a better way forward for future generations.

[1] Following from Ibram X. Kendi’s work in How to be an Antiracist, policy analysis can and should focus on the impact of policy choices on outcomes and whether those outcomes lead to differences by race and ethnicity rather than focusing on intent: explicit or implicit.

[2] Special Data Request, January 2021, Institute on Taxation and Economic Policy.

[3] Erica Williams and Cortney Sanders, “3 Principles for an Antiracist, Equitable State Response to COVID-19 — and a Stronger Recovery,” Center on Budget and Policy Priorities, May 21, 2020, https://www.cbpp.org/research/state-budget-and-tax/3-principles-for-an-antiracist-equitable-state-response-to-covid-19.

[4] Palma Joy Strand and Nicholas Mirkay, “Racialized Tax Inequity: Wealth, Racism, And The U.S. System of Taxation,” Northwestern Journal of Law & Social Policy 15, no. 3 (April 1, 2020): 265.

[5] Special data analysis by Institute on Taxation and Economic Policy. Unit of analysis is non-elderly tax units.

[6] Special data analysis by Institute on Taxation and Economic Policy. Unit of analysis is non-elderly tax units.

[7] Valerie Wilson and William M. Rodgers III, “Black-White Wage Gaps Expand with Rising Wage Inequality,” Economic Policy Institute (blog), September 20, 2016, https://www.epi.org/publication/black-white-wage-gaps-expand-with-rising-wage-inequality/.

[8] Robert Manduca, “Income Inequality and the Persistence of Racial Economic Disparities,” Sociological Science 5 (2018): 182–205, https://doi.org/10.15195/v5.a8.

[9] Ibid.

[10] Special data analysis by Institute on Taxation and Economic Policy. Unit of analysis is non-elderly tax units.

[11] Institute on Taxation and Economic Policy, “North Carolina: Who Pays? 6th Edition,” ITEP, accessed March 9, 2021, https://itep.org/north-carolina/.

[12] Special data analysis by Institute on Taxation and Economic Policy. Unit of analysis is non-elderly tax units.

[13] Special data analysis by Institute on Taxation and Economic Policy. Unit of analysis is non-elderly tax units.

[14] Special data analysis by Institute on Taxation and Economic Policy. Unit of analysis is non-elderly tax units.

[15] Special data analysis by Institute on Taxation and Economic Policy. Unit of analysis is non-elderly tax units.

[16] Bloomberg Markets and Finance, Income Inequality Holds Back Economy Says Fed Chair Powell, 2020, https://www.youtube.com/watch?v=VmOS4MnloUE.

[17] 60 Minutes, Fed Chair Jerome Powell on Income Disparity, 2019, https://www.youtube.com/watch?v=kI9IcSnaWyU.

[18] Sally Golding, “Why Tax Matters,” Tax Justice Toolkit, January 2011, https://taxjusticetoolkit.org/why-bother-with-tax/why-tax-matters/#c101.

[19] “Tax Principles: Building Blocks of a Sound Tax System,” ITEP, accessed March 18, 2021, https://itep.org/tax-principles-building-block-of-a-sound-tax-system/.

[20] “Race and the Lack of Intergenerational Economic Mobility in the United States,” Equitable Growth (blog), February 18, 2020, http://www.equitablegrowth.org/race-and-the-lack-of-intergenerational-economic-mobility-in-the-united-states/.

[21] Ezra Levin, “Federal Policy Brief: Upside Down — Tax Incentives to Save & Build Wealth | Prosperity Now,” January 2014, https://prosperitynow.org/resources/federal-policy-brief-upside-down-tax-incentives-save-build-wealth.

[22] Christopher Otrok, Michael T. Owyang, and Laura E. Jackson, “Tax Progressivity, Economic Booms, and Trickle-Up Economics,” 2019, https://doi.org/10.20955/wp.2019.034.

[23] Vanessa Williamson, “The Long Shadow of White Supremacist Fiscal Policy,” Tax Policy Center, accessed March 30, 2021, https://www.taxpolicycenter.org/publications/long-shadow-white-supremacist-fiscal-policy/full.

[24] Michael Leachman et al., “Advancing Racial Equity With State Tax Policy,” Center on Budget and Policy Priorities, November 15, 2018, https://www.cbpp.org/research/state-budget-and-tax/advancing-racial-equity-with-state-tax-policy.

[25] The People’s Party of North Carolina, “The Proposed Suffrage Amendment. The Platform and Resolutions of the People’s Party,” Documenting the American South, 1899, https://docsouth.unc.edu/nc/populist/populist.html.

[26] Ethan Roy, “Deep Rooted: A Brief History of Race and Education in North Carolina,” EducationNC, August 11, 2019, https://www.ednc.org/deep-rooted-a-brief-history-of-race-and-education-in-north-carolina/.

[27] Ned Cline, “HOW SANFORD’S “TEMPORARY’ FOOD TAX BECAME PERMANENT 35 YEARS AGO,” Greensboro News and Record, May 28, 1996, https://greensboro.com/how-sanfords-temporary-food-tax-became-permanent-35-years-ago/article_7fe343a0-f501-50d8-9b98-fc9c5701574e.html.

[28] Alexandra Forter Sirota, “Income Tax Rate Cap Amendment Is Costly for Taxpayers, Communities,” September 2018. https://www.ncjustice.org/wp-content/uploads/2018/12/BTC-REPORT-tax-amendment-2018.pdf.

[29] “2013 Tax Cuts Worsen Racial Wealth Inequities in North Carolina,” Center on Budget and Policy Priorities, accessed March 30, 2021, https://www.cbpp.org/2013-tax-cuts-worsen-racial-wealth-inequities-in-north-carolina.

[30] Reversing the constitutional amendment would take another legislative-referred ballot measure and a majority vote of the people.

[31] Sydney Idzikowski, Luis Toledo, and Suzy Khachaturyan, “Falling Public Health Investments Show Health Is Not a Priority in N.C.,” October 13, 2018, https://www.ncjustice.org/publications/falling-public-health-investments-show-health-is-not-a-priority-in-n-c/.

[32] “State-Level Life Expectancies by Age by Race/Ethnicity,” State Government, North Carolina Department of Health and Human Services, 2019, https://schs.dph.ncdhhs.gov/data/lifexpectancy/2017-2019/North%20Carolina%202017-2019%20Life%20Expectancies%20by%20Race-Ethnicity.html.

[33] William Munn, “Equity, North Carolina, and the Vaccine – North Carolina Justice Center,” North Carolina Justice Center, February 26, 2021, https://www.ncjustice.org/publications/equity-north-carolina-and-the-vaccine/.

[34] Child Care Services Association, “2019 North Carolina Early Care and Education Workforce Study: ECE Child Care Center Compensation,” November 2020, https://www.childcareservices.org/wp-content/uploads/CCSA_2020_Compensation_Brief_final.pdf.

[35] Rebecca Ullrich, Katie Hamm, and Rachel Herzfeldt-Kamprath, “Underpaid and Unequal,” Center for American Progress, August 26, 2016, https://www.americanprogress.org/issues/early-childhood/reports/2016/08/26/141738/underpaid-and-unequal/.

[36] Martine Aurelien and Alexandra Forter Sirota, “The Missed Opportunity for North Carolina’s Youngest Children,” July 19, 2019, https://www.ncjustice.org/publications/the-missed-opportunity-for-north-carolinas-youngest-children/.

[37] “Racial Disparities Among Extremely Low-Income Renters,” National Low Income Housing Coalition, April 15, 2019, https://nlihc.org/resource/racial-disparities-among-extremely-low-income-renters.